When Connecticut State Senator Doug McCrory got his first credit card after college, he maxed it out in just three weeks [1].

Unfortunately, he was not alone. When it comes to debt, Americans have been treading in dangerous waters for many years, but since the economic crisis of 2008, things have only gotten worse. As of 2019, the collective credit card debt of the entire country reached 1.08 trillion dollars- and that doesn’t include mortgages, student loans, or car loans [2].

Being in debt in America is not a new idea, or even necessarily a bad one. It allows us to buy homes and cars, send our kids to school, and make purchases without having to pay all of the money upfront. But these numbers are staggering, and it seems we’ve gone too far in that direction.

Yet with the financial problems in which so many Americans find themselves, financial literacy has remained conspicuously absent from our school curriculums. This has left many people to ask the question: “why are our children spending so much time learning advanced trigonometry and algebra when they have no idea how to do simple financial math?” A business school in New Haven is taking steps to correct that problem.

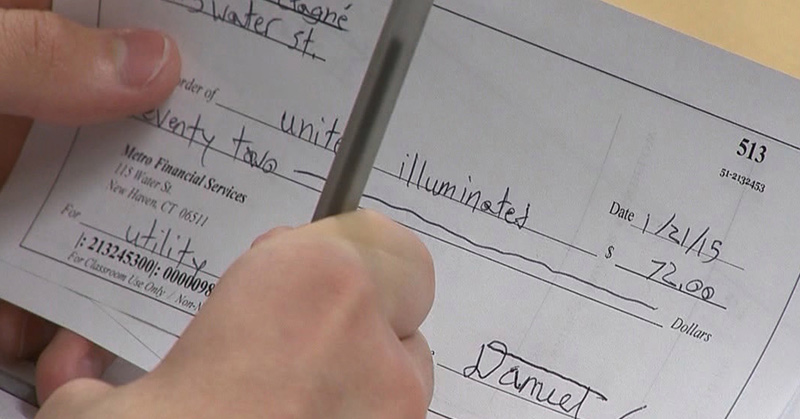

The Jumpstart Program – getting schools teach how to budget money

The school is now offering a course called the Jumpstart program, which is teaching students how to use a calculator, write out a bank check, and balance a budget. They are teaming up with professional financial advisors to deliver the curriculum, in hopes that they will produce a class of financially savvy graduates.

Having taught middle school math for fifteen years, senator McCrory is well aware of the lack of financial knowledge many students possess. This new program is exactly the type of class he wants to see students enrolled in, citing a study done by Champlain College Center for Financial Literacy, which found “that for those students who have a financial literacy course, their credit scores are much better, financially they are doing much better.” He believes that it is about time that Connecticut schools are updating their curriculums with twenty-first-century skill sets [1].

Read: Remembering Typing Class: The Class That Actually Mattered In The Long Run

Financial Math in High School

According to McCrory, there are only seventeen states that require students to take a personal finance course in order to graduate high school. A school in Wethersfield offers a personal finance course as an elective, and it is very popular among both students and their parents.

“We see the course as offering real-word, practical content that students will benefit from regardless of their post-secondary plans.” says school superintendent Michael Emmett [1].

McCrory is hoping that lawmakers will vote to make financial literacy a mandated course, starting in middle schools.

“Introducing it into the curriculum at an early age so that by the time they get to high school they will be ready for it,” he said. “They will know what credit is, they will know what interest rate is.” [1]

Read: ‘Adulting 101’ The High School Class That Teaches Real-World Survival Skills That’s Going Viral

Financial Literacy in the United States

A course such as this could not come soon enough.

Every three years, the Financial Industry Regulatory Authority (FINRA) conducts a survey to assess the personal financial literacy of Americans, and the results have not been stellar.

The survey asks five questions based on key topics such as interest rates, inflation, bonds, mortgages, and risk, and over the last ten years, Americans’ scores have been dropping. As a country, the U.S. ranks fourteenth globally, with a score of 57 percent.

This lack of financial knowledge is having a profound impact on our younger generations. According to the survey, 76 percent of Millennials lack basic financial knowledge, and 70 percent of them are stressed and anxious about saving for the future, knowing how to invest money, and sticking to a budget [3].

Not Just Younger Generations

But it’s not just the younger generations that have a problem- two-thirds of American adults are incapable of passing a basic financial test. Without basic financial skills, it is nearly impossible for Americans to plan for the future, save for retirement, and ensure they have a safety net in case of emergencies [4].

This could have a very real impact on their livelihood. Nearly half of all Americans do not have enough money to cover an unexpected emergency of four hundred dollars or more. 43 percent of student borrowers are not making payments on their loans. 38 percent of households in the United States are carrying some amount of credit card debt, with the average amount being over sixteen thousand dollars [4,5].

To make matters worse, nearly sixty percent of Americans have less than ten thousand dollars saved for retirement, and one in three of them have no retirement savings at all [6]. This is highly problematic because with people living longer coupled with rising healthcare costs, the savings required for retirement are also going up. On top of that, pensions are no longer commonplace the way they once were, and the Social Security Trust Fund, which acts as a safety blanket for many Americans, is on track to be completely depleted within the next fifteen years [4.7].

Fixing the Problem and getting schools to teach how to budget money

Most experts agree- a major way to reverse this problem is to bring financial literacy into the classroom. If financial math is not being taught in schools, the responsibility falls on the individual to educate themselves, but most people don’t understand how important financial skills are until it’s too late.

McCrory is pleased to see schools in Connecticut taking steps to educate their children early about the importance of financial literacy, and he believes that this investment will benefit them in the long run. Knowing that he himself learned these skills a little too late, he hopes that future generations will be equipped with the knowledge to make better financial decisions.

Keep Reading: China promotes education drive to make boys more ‘manly’

Sources

- “State leaders pushing to teach all students how to budget money, balance a checkbook in high school.” WTNH. Jodi Latina. January 24, 2020.

- “Key Figures Behind America’s Consumer Debt.” Debt. Bill Fay. May 13, 2021.

- “America’s Growing Financial Literacy Problem.” Visual Capitalist. Jeff Desjardins. October 28, 2018.

- “4 Stats That Reveal How Badly America Is Failing At Financial Literacy.” Forbes. Dani Pascarella. April 3, 2018.

- “Here’s the average American’s credit card debt — and how to get yours under control.” USA Today. Matthew Frankel. January 24, 2017.

- “1 in 3 Americans Has Saved $0 for Retirement.” Money. Elyssa Kirkham. March 14, 2016.

- “What Happens If the Social Security Trust Fund Runs Out in 2034?” Money. Pat Regnier. July 22, 2015.